There’s a line Michael Preysman once gave to The New Yorker that captures the early Everlane perfectly: “You do not get laid in Everlane.” He meant it as a boast. The clothes were clean, unfussy, almost aggressively unpretentious, the fashion equivalent of showing your work on a math test. No markup mystery. Just a well-made T-shirt and a breakdown of exactly what it costs to produce.

That was the pitch. And for a remarkable window of time in the 2010s, it worked.

Now, in May 2026, Everlane is being sold to Shein, the Chinese ultra-fast-fashion platform that Yale researchers have labeled the biggest polluter in the fast fashion industry, a company that has faced credible accusations of forced labor in its supply chain, fines in Italy for misleading environmental claims, legal challenges in Germany, and a lawsuit from the Texas Attorney General. The deal values Everlane at approximately $100 million. Common stockholders will receive nothing. The $90 million in liabilities that majority owner L Catterton carried on the company’s behalf will be retired by the sale price, meaning the brand effectively traded for the cost of its own debt.

The irony of this acquisition is too obvious.

The Origin Story

Michael Preysman was 25 years old and working in private equity when he noticed something that struck him as a form of consumer fraud hiding in plain sight. Fashion brands were marking up garments five to ten times their production cost, and nobody was saying so. Shoppers paid $80 for a T-shirt that cost $8 to make, and the gap in between the labor, the fabric, the duties, the transport, and the profit margin was invisible by design.

Preysman’s response, in 2010, was Everlane. He and co-founder Jesse Farmer, a developer who built the technical backbone, launched the company from San Francisco with a single product: a $15 cotton T-shirt. But rather than just selling the shirt, Preysman did something fashion had long considered unthinkable. He published a full cost breakdown alongside it: the total cost to make the shirt was $6.70, covering cotton, cutting, sewing, dyeing, finishing, and transport against a retail price of $15, meaning Everlane’s markup was $8.30. There, it was not just the garment, but the logic behind the garment.

The company was launched by invitation only. With an inventory of just 1,500 T-shirts, it started a waitlist that gained 60,000 sign-ups in days. It felt less like a clothing brand than a correction. For a generation of millennial shoppers who had grown up watching corporations sell them stories while hiding the machinery behind the stories, Everlane offered something genuinely novel: trust with receipts.

Early funding came from Kleiner Perkins, Lerer Hippeau Ventures, SV Angel, and Maveron, among others. By 2015, annual sales had reached roughly $35 million. By 2016, they were approaching $100 million, and a Series D round led by Light Street Capital at a reported valuation of around $250 million signaled that investors were fully bought in. The company expanded beyond T-shirts into cashmere, denim, footwear, and outerwear, all presented with the same cost-breakdown transparency. In 2017, it opened its first physical retail store in New York’s SoHo. In 2018, San Francisco followed. The stores were beautiful, minimal, light-filled, very on-brand.

The brand was also genuinely cool. It fit in with the normcore aesthetic, the Kinfolk-magazine minimalism, the aspirational-but-understated lifestyle that defined a particular strain of millennial urban culture. It slid into fashion editorial and Instagram feeds without trying. It attracted loyalty that most fashion brands spend decades and hundreds of millions of dollars attempting to achieve.

And crucially, Everlane seemed to actually believe what it was saying. In 2019, a reporter visited the San Francisco headquarters and found a company kitchen stocked with food in minimal packaging, a team that regularly visited overseas factories and planted community gardens, and a sustainability director who walked through the specific challenges of moving garments through the supply chain without sealing each one in a separate plastic bag. The people running Everlane weren’t just marketing ethics; they appeared to be practicing them.

The Seeds of Drift

But even in the good years, something more complicated was developing beneath the surface.

The “radical transparency” that Everlane trademarked turned out to be selective by design. The company was meticulous about price transparency, showing you the production cost of a sweater but far less forthcoming about wages, working conditions, and raw material sourcing. Watchdogs and sustainability researchers began to notice the gap between what Everlane disclosed and what it didn’t. Disclosing a factory’s location tells you almost nothing about how the workers there are being paid. Showing a production cost breakdown tells you nothing about whether the people behind that cost are thriving or just surviving.

Nonprofit organizations that audit fashion brands began flagging Everlane for what they called greenwashing: the practice of marketing yourself as ethical and eco-friendly without fully living up to the claims. One organization placed Everlane among fashion’s worst greenwashers in December 2020, pointing to undisclosed factory conditions, absence of worker pay data, and limited third-party verification of the supply chain.

There was also the structural contradiction at the heart of the model: ethical supply chains are expensive to maintain. Organic cotton costs more than conventional cotton. Responsibly certified mills charge more than uncertified ones. Keeping those standards while also satisfying investors who paid escalating valuations for the company required either raising prices (which eroded the “honest value” positioning) or cutting corners on the standards (which eroded the ethical positioning). Neither option was good.

The Growth Trap

The more insidious problem was what growth itself did to the company’s identity.

Preysman had famously told reporters that he would rather shut Everlane down than open physical retail stores. The DTC model was the product, not just a distribution channel, but the whole premise of the brand. No middlemen or no markups and no fixed costs bleeding the margins that the company had positioned as honest and clean. When Everlane reversed course and opened stores in New York in 2017 and San Francisco in 2018, it wasn’t just a strategic pivot but a business repositioning.

The stores were signed as leases, staffed with employees, built out with capital, and maintained with fixed costs at exactly the moment when the economics of small-format physical retail were becoming difficult for brands without enormous wholesale distribution to support them. The company had adopted the overhead of a conventional retailer while retaining the margin structure of an ethical brand and the revenue base of a DTC startup. That combination was quietly ruinous.

The expansion of the product line compounded the problem. What began as a tight edit of high-quality essentials, the T-shirts, cashmere, and denim that had defined Everlane’s identity, grew into activewear, swimwear, shoes, bags, outerwear, celebrity collaborations, and limited capsule collections. Each new category required new supplier relationships to audit, new factories to vet, and new material certifications to maintain. The transparency promise that was entirely manageable for five products became increasingly unmanageable for fifty. The brand that had made its name by showing its work couldn’t show all of it anymore; there was simply too much of it.

Customers noticed it. The quality perception that had been central to Everlane’s value proposition, a product so well-made it justified the honest markup, started to erode. Longtime loyalists who had paid $15 for a T-shirt that lasted five years found themselves paying $35 for something that didn’t feel as carefully considered. The products were still good, often quite good. But the magic of the early years, the sense that each item had been chosen with exceptional care and presented with exceptional honesty, was harder to find in a catalog of hundreds of SKUs.

The Private Equity Ratchet

When L Catterton led an $85 million investment in 2020, announced at the time as a minority stake but one that would give the PE firm effective majority control, investing at a $550 million valuation, the structural pressures on the company shifted into a different register entirely.

Private equity operates on a simple logic: you acquire a company at a valuation, you grow it beyond that valuation, and you exit. The gap between entry and exit is the return. L Catterton had put in $85 million at $550 million, which meant Everlane now needed to become worth considerably more than $550 million within a defined window to make the investment worthwhile. That kind of expectation doesn’t coexist easily with the patient, careful approach that ethical sourcing demands. It creates pressure to pursue premium repositioning, expand margins, and grow faster than the supply chain can responsibly absorb.

At around the same time, Preysman stepped back from day-to-day leadership, transitioning to an executive chairman role focused on climate. Andrea O’Donnell, formerly of Deckers Brands, was brought in as CEO to run operations. Preysman would be the last of Everlane’s leaders to have the institutional knowledge of what the brand had been built to be. What followed was a succession of CEOs, O’Donnell, then Alfred Chang from streetwear brand Fear of God, each attempting to steady a company that kept losing altitude.

2020: The Year Everything Cracked Open

The pandemic arrived not as the cause of Everlane’s troubles but as the moment that made them impossible to ignore.

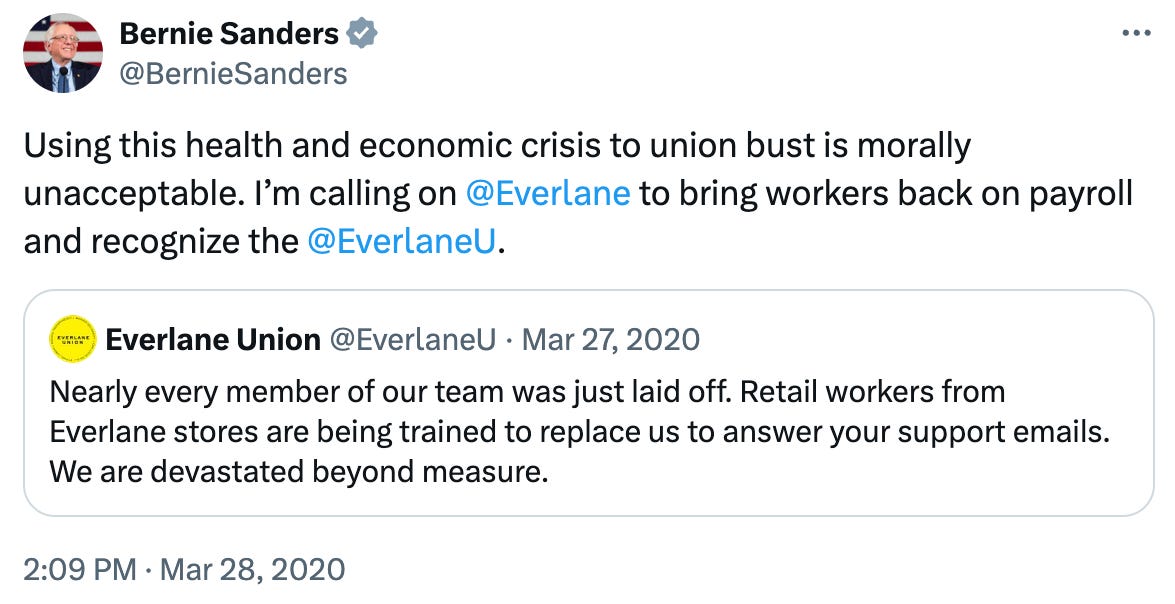

In December 2019, Everlane’s Customer Experience team announced its intention to unionize. The workers who answered customer emails and calls were classified as part-time contractors, with hours capped at 29 per week to keep them just below the threshold that would require the company to provide health benefits organized under the banner of a brand whose mission statement was built on doing right by people.

When the pandemic hit in March 2020 and Everlane’s retail stores closed overnight, the company laid off hundreds of those workers. The timing was catastrophic for the brand’s reputation. Senator Bernie Sanders publicly condemned the move. “Using this health and economic crisis to union-bust is morally unacceptable,” he wrote. Workers who said they had been told in the days beforehand that the company was “in this together” found themselves let go in a mass termination.

Everlane maintained that the layoffs were about survival, not union suppression. But the optics were devastating for a brand whose entire identity rested on the claim that it treated its workers differently from everyone else in fashion.

Months later, a group of former Black employees who called themselves the “Everlane Ex-Wives Club” published a public letter alleging a culture of systemic racism inside the company, accusing leadership of “convenient transparency,” a phrase that cut straight to the heart of what critics had been saying for years. The brand had built enormous goodwill among customers who associated ethical consumption with social justice broadly defined. The letter torched that credibility from the inside.

Following an apology and internal investigation, Everlane changed leadership and began publishing annual impact reports. But the damage to the brand’s foundational mythology, the sense that Everlane was genuinely different, that it wasn’t just marketing ethics but practicing them, proved very difficult to repair.

The Slow Bleed

What followed was a long, grinding slide that unfolded in stages over the next five years.

Gross margins improved when O’Donnell and Preysman nudged up prices and worked on sourcing efficiencies, rising from 60 to 70 percent. But revenue flatlined. Online sales accounted for roughly 80 percent of the business, and they were volatile month to month. Physical retail provided some growth, but not enough to offset the fixed costs it introduced. The company cut 17 percent of its corporate workforce in January 2023, citing inflation and recession fears.

By late 2022, Everlane had taken on $90 million in new debt financing: a $65 million revolving credit facility from CIT Northbridge and a $25 million loan from Gordon Brothers. That debt would become the defining fact of the company’s final years, a number that appeared in every conversation about the brand’s future and eventually determined the terms of its sale.

The company tried pivots. It shifted its messaging from “radical transparency” to “clean luxury,” an attempt to reposition toward premium consumers and rebuild trust after the scandals. It partnered with Nordstrom in 2024 for shop-in-shop arrangements, taking the brand into wholesale channels it had once rejected on principle. It brought in Alfred Chang and began experimenting with designer collaborations and celebrity partnerships to generate cultural heat.

None of it worked well enough, or quickly enough. By early 2026, Everlane was being sued to vacate its San Francisco headquarters after failing to pay $51,000 in overdue rent. In March, L Catterton began shopping the brand. They were looking for a new co-investor to help retire the debt load, or a buyer willing to take the whole thing off their hands. Along came Shein.

The Sale

The board approved the deal on Saturday, May 16, 2026. The price was $100 million. With $90 million in debt to retire, the equity value was essentially zero for common stockholders, who were told Sunday morning that they would receive no payout.

Everlane had been valued at $550 million in 2020. It had once floated projections of $550 million in annual revenue. Instead, it sold for less than half a year’s sales, at a multiple of roughly 0.5x revenue.

Why did Shein want it? The logic is strategic rather than sentimental. Shein has spent years navigating serious regulatory and political headwinds in Western markets. It has been fined in Italy, challenged in Germany, sued in Texas, and scrutinized by the UK Parliament over its supply chain’s links to forced labor and toxic chemicals. Its IPO ambitions have been complicated at every turn by the ethical questions its core business model generates. Acquiring an American brand with a loyal customer base, a domestic DTC infrastructure, and a decade-long history of ethical positioning gives Shein something it cannot produce in-house: a story about its portfolio that is more palatable than the one its core business tells.

“Ultimately, the deal likely saves Everlane,” said Neil Saunders of GlobalData. “But that salvation comes at a price.”

What It All Means

The reaction has been swift and sharp. Former CTO Nan Yu posted on X: “I haven’t worked at Everlane in almost 10 years, but it’s a pretty sad day for the people that built it.” Customers who had shopped the brand for a decade described the association with Shein as a betrayal.

But the Everlane story is not, at its core, a simple story about hypocrisy. The early team genuinely believed in what they were building. The transparency was real, even if imperfect. The factory relationships, the plastic commitments, the kitchen without packaging, these were not fabrications. Everlane was trying to do something harder than most fashion companies attempt.

It made the same mistakes as every other growth-stage company, just with more public commitments to not making those mistakes.

The same period brought the collapse of nearly every peer in the “millennial DTC” cohort. Allbirds sold its footwear business for $39 million and pivoted to AI infrastructure. Casper, Outdoor Voices, SmileDirectClub, and Winc are all gone or radically diminished.

Even the survivors, like Warby Parker and Glossier, have had to confront the gap between the DTC premium that investors once paid and the margins the businesses can actually generate.

The Everlane sale is the settlement notice for that entire era. It turns out that “sustainable” is not a strategy unless the business itself is built to sustain.

And the company that trademarked “radical transparency” will now be owned by one that has been fined for concealing it.

New article every Tuesday.

Be Bold. Be Real. Be Anomalous.

Follow for more Be Anomalous stories, conversations, and behind-the-scenes.

Website | Instagram | LinkedIn | YouTube | @iamsaimenon

This is an absolute masterclass in brand analysis, Sai. The line, The transparency promise that was entirely manageable for five products became increasingly unmanageable for fifty perfectly diagnoses the growth trap.

Everlane’s tragic end highlights a brutal reality: the traditional fashion supply chain forces brands to choose between scale and ethics. When you scale SKUs, you take on massive upfront inventory debt, and eventually, the private equity ratchet forces you to compromise your values just to feed the machine.

It's exactly why we are seeing a massive shift toward a 'Slow Fashion' pre-order model. By utilizing crowdfunding pre-order drops, independent apparel brands are capping their SKUs, letting consumers pay for their exact sizes upfront, and only manufacturing what is already 100% sold. It keeps inventory debt at zero and completely protects the brand's ethical integrity.

I map out these 3-step launch frameworks specifically to help independent fashion lines scale without falling into this exact Everlane growth trap. Do you think it’s structurally possible for an ethical apparel brand to reach mass-market scale today without taking on the toxic debt that ultimately killed Everlane?